United Parcel Service, Inc. (UPS)

UPS Intrinsic value

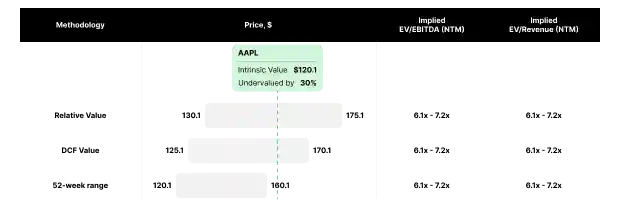

UPS Intrinsic value overview

UPS Historical intrinsic value

UPS Relative value

UPS Valuation multiples overview

UPS vs Peer Set Valuation Multiples Dynamics

UPS DCF sensitivity

UPS Discount rate (WACC)

Discover more UPS fundamentals

FAQ

What is the DCF value of United Parcel Service, Inc. (UPS)?

As of today, DCF Value of United Parcel Service, Inc. is $147.3, which is undervalued by 8.5%, compared to the current market share price of $135.7

How was the DCF Value calculated?

Step 1: Calculating Intrinsic Enterprise Value DCF Value was calculated by estimating United Parcel Service, Inc. future free cash flow and then discounting it, using a chosen discount rate to determine Intrinsic Enterprise Value of $79.8B Step 2: Balance Sheet Adjustments Intrinsic Equity Value is calculated by subtracting Balance Sheet items (Cash & Equivalents, Short-term investments and Total Debt) from previously calculated Intrinsic Enterprise Value. This Intrinsic Equity Value is then divided by the total number of outstanding shares of 852,900,000 to determine DCF Value of $147.3

What is the Relative value of United Parcel Service, Inc. (UPS)?

As of today, Relative Value of United Parcel Service, Inc. is $165.8, which is undervalued by 22.1%, compared to the current market share price of $135.7

How was the Relative Value calculated?

Relative Value was calculated by applying various valuation multiples (EV/Revenue, EV/EBITDA, P/E etc.) to United Parcel Service, Inc. financials to determine Relative Value of $165.8

What is United Parcel Service, Inc. (UPS) discount rate?

United Parcel Service, Inc. current Cost of Equity is 9.4%, while its WACC stands at 8.2%. Cost of Equity is used to value equity, while discounting free cash flow to equity holders (such as Net Income or Free Cash Flow to Equity). Weighted Average Cost of Capital (WACC) is used to value the entire firm, while discounting cash flows available to both debt and equity holders (NOPAT or Free Cash Flow to the Firm)

How is Cost of Equity for United Parcel Service, Inc. (UPS) calculated?

The Cost of Equity represents the return a company must offer investors to compensate for the risk of investing in its stock. It's calculated using the Capital Asset Pricing Model (CAPM), which combines the risk-free rate, the stock's beta, and the equity risk premium (ERP). This model considers the inherent risk of investing in the stock compared to a risk-free investment and the market's overall risk. Cost of Equity = Risk-Free Rate + Beta x Effective Risk Premium (ERP) 9.4% = 4.51% + 1 x 5.0%

How is WACC for United Parcel Service, Inc. (UPS) calculated?

WACC, or Weighted Average Cost of Capital, is a calculation that reflects the average rate of return a company is expected to pay its security holders to finance its assets. It is a critical measure in financial analysis for valuing a company’s entire operations. The WACC formula combines the costs of equity and debt, weighted by their respective proportions in the company's capital structure. WACC = Cost of Equity x Equity Weight in Total Capital + Cost of Debt x (1 - Effective Tax Rate) Debt Weight in Total Capital 8.2% = 9.4% x 83.1% + 3.4% x (1 - 22.7%) x 16.9%